Why Looking at the Seller’s Property Taxes is a Huge Mistake (and How California’s Prop 13 Actually Works)

If you are scrolling through Zillow, Redfin, or Threads looking at homes in San Diego, there is one piece of data on the listing page you need to completely ignore: what the current seller pays in property taxes. I see home buyers make this mistake all the time. They look at a listing, see a beautifully low property tax history, and assume that's what their monthly payment will look like.

Spoiler alert: It won’t. Here is what you actually need to know about how property taxes work in California, how to estimate your real payment, and why we have Prop 13 to thank for keeping us in our homes.

1. The Seller's Tax Bill is Irrelevant to You

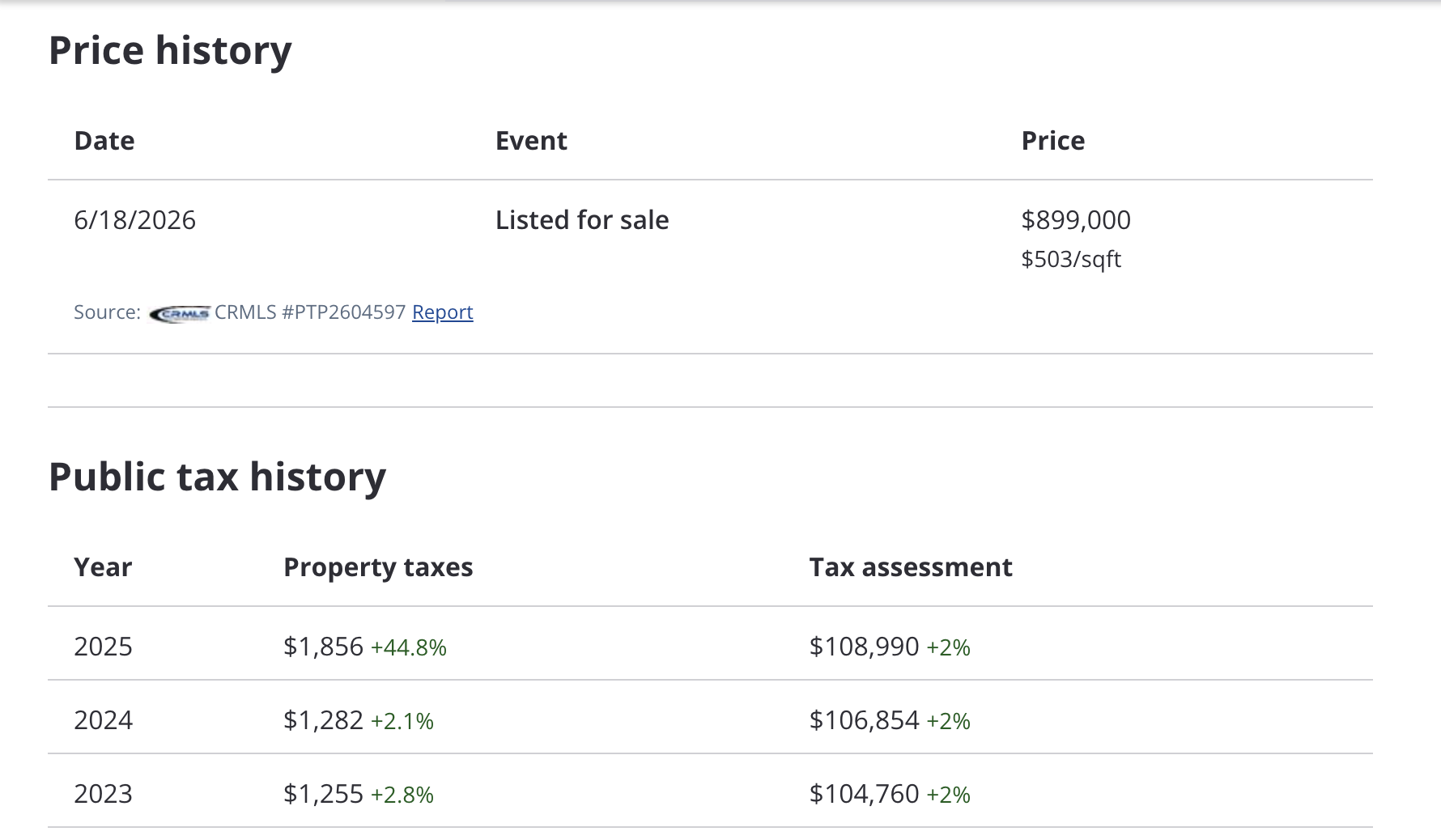

When a home changes hands, the clock resets. Taxes are recalculated based on your purchase price, not what the previous owner was paying.

If the seller bought the home decades ago when it was worth $100,000, they might only be paying $1,000 a year in taxes. But if you are buying that same home today for $900,000, your tax bill is going to look vastly different. Don't base your budget on their history.

2. How to Accurately Estimate Your Taxes

To get a realistic idea of what you’ll actually pay, you need to do some quick math based on your expected purchase price:

-

The Baseline: The California state tax rate is capped at 1%.

-

The Reality: Most counties have passed local bonds and assessments over the years to pay for schools, infrastructure, and other local projects.

-

The San Diego Rule of Thumb: In San Diego County, these extra fees usually push the actual tax rate into the 1.1% to 1.2% range.

Math Tip: To be safe and conservative with your budget, multiply your estimated purchase price by 1.2%. That will give you a highly accurate estimate of your annual tax bill.

3. The Power of Prop 13: Protection for the Future

Once you buy your home and that initial tax bill is set, you get to benefit from one of California’s biggest real estate perks: Proposition 13.

Under Prop 13, your home’s assessed value for tax purposes can only go up by a maximum of 2% per year, regardless of how sky-high the actual housing market goes.

For example, if you buy a $1,000,000 home, the maximum your assessed value can increase the next year is $20,000, meaning your tax bill can only increase by about $240 for that year.

Why this matters (The "Other States" Comparison)

An extra $240 a year might sound like annoying inflation, but compared to the rest of the country, it’s a massive win.

Imagine you bought that $1M home and the market boomed, doubling its value to $2M over six years (which we've seen happen recently!).

-

In other states: Your taxes could be reassessed at the full $2M market value, skyrocketing your annual tax bill from $20,000 to $40,000.

-

In California: Your taxes are protected by that 2% cap.

In many states, wild market appreciation actually forces people—especially retirees or those on fixed incomes—to sell their homes because they literally can no longer afford the property taxes. Prop 13 was put in place specifically to protect Californians from being priced out of their homes.

The Bottom Line

When shopping for a home, look at the purchase price, look at any HOA costs, but ignore the seller's tax bill. Crunch your own numbers at 1.2%, and rest easy knowing that once you buy, Prop 13 has your back.

Categories

Recent Posts

"My job is to find and attract mastery-based agents to the office, protect the culture, and make sure everyone is happy! "